Finance

3 AI stocks for the second half of 2024

The tech bull market, fueled by innovations in generative AI in 2023 continued into the first half of 2024. Even if the focus is on technology in general rather than the sector’s strongest performers, the technology-focused companies remain Nasdaq composite index delivered a total return of almost 19%.

Knowing this, investors may wonder which stocks could take the lead in the second half of the year. While the market offers no guarantees, the last two quarters of the year could be the time when some stocks start to rise in earnest. In this article, three Motley Fool contributors provide insights on stocks they think investors should keep an eye on for the rest of the year.

Alphabet is positioned to leverage its search market dominance for AI wealth

Jake Lerch (alphabet): My choice is Alphabet (NASDAQ: GOOGL) (NASDAQ: GOOG), the parent company of Google. What I really like about Alphabet is that the company combines two of the most critical attributes of any outstanding stock: potential, best represented by its artificial intelligence (AI) tools, and results, as evidenced by its consistent financial performance.

Let’s explore its potential first. When it comes to AI, the sky is the limit for Alphabet. The company’s latest AI-powered personal assistant, Google Assistant, offers many features to help people achieve more. Through voice commands alone, users can:

-

Set timers, create lists and save locationS and passwords.

-

Call, text and read emails.

-

Gather local information such as weather, traffic and directions.

-

Answer general questions, such as “how many grams in an ounce” or “what is 18% of $57.”

-

Search and play music, movies or podcasts.

Moreover, Alphabet may be uppercase on its huge user base. As the most visited website in the world, Google processes more than 8.5 billion searches per day – about one for every person on the planet. As such, Alphabet has a significant opportunity to make Google Assistant the AI assistant of choice. This could lead to significant benefits for Alphabet in the future as it explores ways to monetize Google Assistant through a subscription model where users pay a monthly fee for premium features or an advertising model where companies pay to have their products or services featured by the assistant. have it recommended.

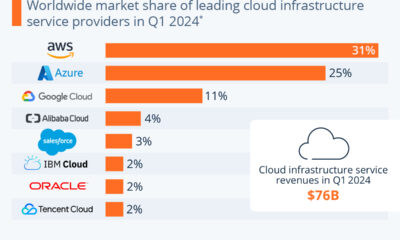

In the meantime, Alphabet can rest assured that its already established businesses, such as Google Cloud, YouTube and Android, will continue to “bring the bacon home.” These companies demonstrate consistent growth and profitability, contributing to Alphabet’s overall stability and investment potential.

In short: Alphabet could be the AI stock to watch in the second half of 2024 – and beyond. Investors looking for a stock with an unbeatable combination of potential and performance would be wise to consider this.

Meta stocks aren’t done riding the AI wave yet

Justin Pope (metaplatforms): Social media giant Metaplatforms (NASDAQ: META) has traveled a rocket-like trajectory. Shares are up 45% since January and are up an astonishing 326% since January 2023, when artificial intelligence started to pick up steam. In just 18 months, Meta Stocks created the magnitude of wealth that the broader market typically takes decades to achieve. I understand if people are skeptical that Meta has more in store.

Still, the fundamentals indicate that Meta could continue on its current momentum in the second half of this year. This is mainly driven by strong operating performance and a share valuation that is still borderline cheap. Meta’s core business is advertising to billions of social media users. Meta is still impressively gaining users even though so many people are already using its apps. Meta’s family of apps, including Facebook, Instagram and WhatsApp, grew to 3.24 billion daily active users in the first quarter, up 7% on annual basis.

Digital advertising continues to take market share away from older media formats such as television and print, so Meta is benefiting from the tailwinds there too. Meta’s ad volume rose 20% year over year in the first quarter. Finally, Meta started using AI to help companies advertise more efficiently, increasing Meta’s price per ad by 6% in the first quarter. In other words, Meta benefits from multiple variables that drive its primary activities.

Investors will have to see how Meta continues to perform in the coming quarters. Analysts are very optimistic; EPS estimates for 2024 of $20.16 would represent 35.5% growth from 2023. Meanwhile, analysts believe Meta will grow earnings by an average of more than 19% per year over the next three to five years. Given the healthy growth prospects, Meta shares remain demonstrably cheap with a price-to-earnings ratio (P/E) of 25.

Meta is a world-class company experienced a serious setback in 2022. The comeback has delivered eye-popping returns. While Meta’s meteoric rise means there is likely much less upside potential than before, investors shouldn’t jump ship too quickly. There is still plenty of wind in the sails.

In AI chips, a rising tide could lift AMD

Will Healy (Advanced micro devices): Datum NvidiaIts dominance in AI chips makes potential competitors easy to ignore at first glance.

However, according to Allied Market Research, the AI chip industry is expected to grow at a compound annual growth rate (CAGR) of 38% through 2032. With Nvidia apparently struggling to meet current demand, it leaves an opening for competitors like Advanced micro devices (NASDAQ: AMD).

While Nvidia is at the forefront of the innovation battle, AMD has a history of catching up and sometimes even surpassing its competitors. While an AI chip from Nvidia costs about $30,000 to $40,000, AMD’s $10,000 to $15,000 semiconductors will likely appeal to customers eager to get their hands on all the AI chips they can find.

More recently, investors have largely overlooked AMD as its $5.5 billion in revenue grew just 2% annually in the first quarter of 2024. However, data center revenue of $2.3 billion increased 80% over the same period. Additionally, it represented 42% of the company’s total revenue, a level comparable to Nvidia’s percentage of data center revenue at the end of fiscal 2022 (ending January 30, 2022) of 39%.

Fast forward to the first quarter of 2025 (ending April 28), and 87% of Nvidia’s revenue came from the data center segment. With AMD’s aforementioned 80% data center growth, Nvidia’s recent history shows how AMD could follow in its footsteps if AI chips become the dominant source of revenue.

Moreover, Nvidia’s revenue, mainly driven by AI chips, grew 262% annually in that quarter. While AMD may or may not match that number over time, Nvidia’s recent history details what could happen to AMD’s revenue growth as sales of AI chips increase.

Furthermore, AMD has a significant valuation advantage when we look beyond its misleading price-to-earnings ratio of 232. The company currently trades at a price-to-book ratio of around 4.5. By comparison, Nvidia is selling at 63 times book value. This difference makes AMD stock a relative bargain, freeing up inventory space as AI chip sales become a more critical revenue stream.

Should you invest €1,000 in Alphabet now?

Before you buy shares in Alphabet, consider the following:

The Motley Fool stock advisor The analyst team has just identified what they think is the 10 best stocks for investors to buy now… and Alphabet wasn’t one of them. The ten stocks that survived the cut could deliver monster returns in the coming years.

Think about when Nvidia created this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $757,001!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates, and two new stock picks per month. The Stock Advisor is on duty more than quadrupled the return of the S&P 500 since 2002*.

*Stock Advisor returns June 24, 2024

Randi Zuckerberg, former director of market development and spokeswoman for Facebook and sister of Mark Zuckerberg, CEO of Meta Platforms, is a member of The Motley Fool’s board of directors. Suzanne Frey, a director at Alphabet, is a member of The Motley Fool’s board of directors. Jake Lerch has positions in Alphabet and Nvidia. Justin Pope has no position in any of the stocks mentioned. Will Healy has positions in Advanced Micro Devices. The Motley Fool holds positions in and recommends Advanced Micro Devices, Alphabet, Meta Platforms, and Nvidia. The Motley Fool has one disclosure policy.

3 AI stocks for the second half of 2024 was originally published by The Motley Fool