Finance

A recession puts the markets at risk, but is not yet alarming

By Yoruk Bahceli and Dhara Ranasinghe

(Reuters) – Disappointing U.S. jobs data has shaken confidence in a soft landing for the world’s largest economy, sending global stock markets tumbling and betting on interest rate cuts soaring.

But investors who have abandoned the popular carry trade in the yen have played a major role in the sell-off, complicating the message of asset prices on the economic outlook.

The likelihood of a recession is anyone’s guess. Goldman Sachs has increased the chance of a US recession to 25%. JPMorgan sees a 35% chance of a start before the end of the year.

Here’s what five closely watched market indicators say about the risks of a global recession:

1/ DATA PUZZLE

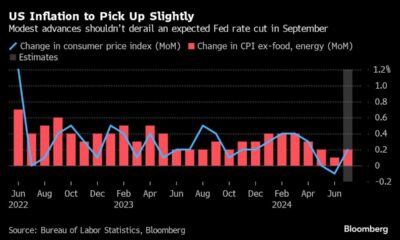

The US unemployment rate rose near a three-year high of 4.3% in July, due to a significant slowdown in hiring.

It stoked fears of a recession by hitting a trigger point of the ‘Sahm rule’, which has historically shown that a recession is coming when the three-month moving average unemployment rate is half a percentage point above the low of the previous 12 months rises.

Still, many economists believe the reaction to the data was overblown, as the numbers may have been skewed by immigration and Hurricane Beryl. Better-than-expected jobless claims data on Thursday also supported this view, sending stocks higher.

“Payrolls are still growing. If you saw payrolls going negative, I would be much more concerned about a real recession starting,” said Dario Perkins, managing director, global macro at consultancy TS Lombard.

The U.S. economy grew at an annual rate of 2.8% in the second quarter, double the rate in the first quarter and on par with the pre-pandemic average. Activities in the services sector also indicate continued growth.

However, outside the United States, business activity indicators point to faltering growth in the eurozone, while China’s recovery remains fragile.

Global economic data is delivering negative surprises approaching the highest rate since mid-2022, according to Citi’s surprise index.

2/ BUSINESS ROUTE

MSCI’s global stock index is down more than 6% from July’s record highs, while the US S&P 500 has lost more than 4% so far in August.

Still, analysts believe the shares, which are still up about 7% globally this year, are far from heralding a recession.

Goldman Sachs estimates that any further sell-off of 10% of US stocks would reduce growth by just under half a percentage point over the next year.

Credit terms could prove more important, analysts say.

They note that while the risk premium that corporate bonds pay over government bonds has increased in Europe and the United States, it was correcting from historically tight levels and the movements were not yet pronounced enough to suggest that the risk on a recession was big.

According to BofA, recession expectations, which stem from the gap between US investment grade bond yields and government bond yields, are about half as high as they would be in the 2022-2023 period.

3/ CUT AWAY

Spurred by US employment data and a dovish-sounding Federal Reserve, traders are now pricing in around 100 basis points of cuts in US interest rates by the end of the year.

That is less than the more than 130 basis points earlier this week, but double the roughly 50 basis points expected on July 29. Markets are also pricing in a greater than 50% chance of a significant cut of 50 basis points in September.

The big banks also added the Fed cuts they expect this year.

Steve Ryder, portfolio manager at Aviva Investors, said the Fed was likely to cut rates three times this year, but given the uncertainty over the development of economic data, it was understandable that markets were assessing the likelihood that it would have to cut further.

Elsewhere, traders see a high chance of three more rate cuts from the European Central Bank this year, after seeing less than a full chance of a second cut in mid-July.

4/ EFFICIENCY CURVE

Rate cuts have pushed shorter-term U.S. Treasury yields lower and the closely watched part of the yield curve that tracks the gap between 10- and 2-year Treasury yields closed Monday for the first time since July 2022 became positive.

Although a yield curve inversion has historically been seen as a good predictor of a recession on the horizon, the curve tends to return to normal as the recession approaches.

However, with the curve inverted for a record time in this cycle and no recession in sight, a majority of strategists Reuters surveyed earlier this year no longer consider this a reliable recession indicator.

Since then, the curve has inverted and stood at minus 5 basis points on Thursday.

5/ DR-BUYER

Known as “Dr Copper” for its track record as a boom-bust indicator, it posts the metal to a 4.5-month low this week, putting it firmly on the recession list.

Three-month copper prices on the London Metal Exchange, trading around $8,750 a tonne, have fallen about 20% from May’s record high, reflecting pessimism about the global economic outlook.

Oil prices, another barometer of the health of global demand, are near year-to-month levels. But their decline was limited by concerns that tensions in the Middle East could undermine supplies from the biggest oil-producing region.

(Reporting by Yoruk Bahceli and Dhara Ranasinghe; Editing by Tomasz Janowski)