Finance

The S&P 500’s Winning Streak Faces the ‘Bad September’ Test: Markets Shut Down

(Bloomberg) — Stocks rose at the end of a wild August on Wall Street, as investors braced for what has historically been known as the worst month for stocks.

Most read from Bloomberg

Despite all the whiplash in global markets just a few weeks ago, things are looking relatively calm. Stocks saw mild moves on Friday, with the S&P 500 poised for a fourth straight monthly gain amid data showing the economy is holding up, while the door remained open for the Federal Reserve to start cutting rates in September. As for whether there is still a massive reduction, next week’s jobs report could provide some clues.

“As August draws to a close, sentiment has calmed considerably compared to the start of the month,” said Nationwide’s Mark Hackett. “Many of the bigger concerns in the overall economy have subsided. September may bring some seasonal challenges, but if investors can navigate them, these challenges could turn into advantages in the fourth quarter.”

Since 1950, the S&P 500 has generated an average loss of 0.7% in September and finished higher only 43% of the time, making it the worst month for stocks based on average return and positivity, according to Adam Turnquist LPL Financial. The past four Septembers have also been notably weak, with the index down 4.9%, 9.3%, 4.8% and 3.9% respectively.

“During the month, the index tends to trade sideways during the first half, with losses starting to pile up until the end of the month,” he said. “For this year, the midpoint also happens to closely align with the Fed’s September meeting.”

The S&P 500 rose to about 5,610 points. Volume was thin ahead of Monday’s US holiday. The Nasdaq 100 added 0.7%. The Russell 2000 of small companies was little changed. Wall Street’s “fear gauge” – the VIX – fell to around 15. That’s after an unprecedented spike that took the index above 65 during the August 5 market sell-off.

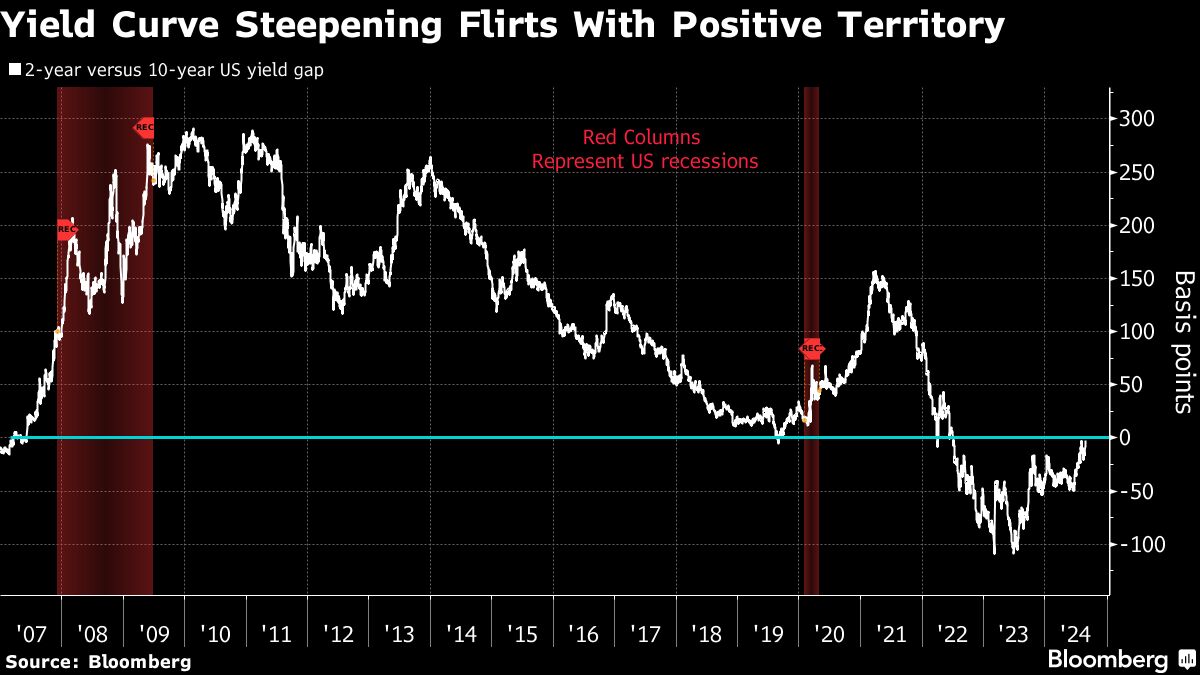

Treasury bonds fell, but were poised for their longest monthly winning streak since 2021. The dollar rose at the end of the year’s worst month. Oil prices fell as traders factored in expectations that OPEC+ will continue with previously announced production increases in the fourth quarter.

Stock bulls tried to end August “with a bang” but were met with near-record selling pressure ahead of what has historically been the worst month for stocks, according to Interactive Brokers’ Jose Torres.

Data from Bespoke Investment Group shows that September has also been by far the worst month of the year for the Dow Jones Industrial Average over the past 100 years, with an average decline of 1.24%. An analysis of data from Citigroup Inc. since 1928, the S&P 500’s average realized volatility for September has historically been 1.5 points above August, while October was another 2.5 points higher.

There are a few theories as to why September is typically a weaker month for stocks. For starters, investors returning from summer vacations tend to defensively reassess their portfolio positioning. Companies prepare their budgets for the coming year and debate belt-tightening. And mutual funds often engage in “window dressing” by selling positions at a loss to reduce the size of their capital gains distributions.

“Additionally, companies that enter a stock buyback blackout period at the end of the third quarter could impact their ability to support their share price if the price declines,” Hackett said.

For now, many traders are pinning their hopes on more data that will show the economy isn’t falling off a cliff as inflation continues to march toward the Fed’s 2% target.

A report on Friday showed U.S. consumer confidence improved for the first time in five months as lower inflation and the prospects of Fed cuts helped raise expectations about personal finances. The Fed’s favorite measure of underlying U.S. inflation — the main price index for personal consumer spending — rose at a mild pace.

“This week’s data puts to rest concerns about recession and inflation,” said David Russell of TradeStation. “Goldilocks could be here as Jerome Powell prepares to turn the page.”

Powell said last week that the time has come for the central bank to cut its key policy rate. In doing so, he confirmed expectations that officials will start cutting borrowing costs next month and made clear that he intends to prevent a further slowdown in employment.

Like the Fed, investor focus appears to be shifting from inflation to the labor market, and soon all eyes will be on next Friday’s monthly jobs report, according to eToro’s Bret Kenwell.

“Last month’s jobs report was a big miss, raising widespread concerns that the Fed was late in cutting rates,” he noted. “Another big miss could increase speculation of a 50 basis point cut versus the current expectation of a 25 basis point cut.”

According to strategists at Barclays Plc, equity markets are likely to benefit again from good economic data, which is needed to extend the rally beyond the technology sector.

The team led by Emmanuel Cau says monthly US jobs figures next week will be the benchmark for confirming or refuting recession concerns.

“If it is a bad print, stocks would undoubtedly react poorly given their post-recovery levels,” they wrote. On the other hand, a better-than-expected figure “would help allay fears of a near-term recession and is likely good for stocks.”

Swap contracts are fully priced into a quarter-point move and a roughly 25% chance of the half-point cut predicted by at least two major U.S. banks. They remain almost fully pricing in a half-point rate cut this year, anticipating a cumulative easing of nearly 100 basis points over the Fed’s three remaining policy meetings.

“Markets are now waiting for next week’s labor market data, which should determine whether the Fed opens the rate cut with a cut of 50 or 25 basis points – the difference between an emergency cut and a normalization cut,” said Florian Ielpo of Lombard Odier. Investment managers.

Cash funds recorded inflows of about $24.5 billion in the week through Aug. 28, a fourth straight week of additions, according to a note from Bank of America Corp., citing EPFR Global data. About $20.7 billion went into bond funds, while $13.7 billion flowed into stocks, the data showed.

US stocks rose for the ninth week in a row, reaching $5.8 billion.

Business highlights:

-

Intel Corp. is working with investment bankers to help it weather the toughest period in its 56-year history, according to people familiar with the matter.

-

The company is discussing various scenarios, including a split of its product design and manufacturing operations, and which factory projects might be scrapped, said the people, who asked not to be identified because the deliberations are private.

-

-

Dell Technologies Inc. reported better-than-expected revenue due to an increase in sales of servers built to handle artificial intelligence workloads.

-

Lululemon Athletica Inc. lowered its sales and profit outlook for the year as increased competition and brutal inflation curb demand for its pricey yoga pants.

-

Ulta Beauty Inc. lowered its sales forecasts as more U.S. consumers cut back on makeup and cosmetics due to higher prices and higher borrowing costs.

-

Autodesk Inc. raised its full-year profit outlook after pressure on the software maker from activist investor Starboard Value LP.

-

The Alnylam Pharmaceuticals Inc. trial with its drug to treat a fatal form of heart disease fell short of investor expectations.

Some of the major moves in the markets:

Stocks

-

The S&P 500 rose 0.4% as of 2:48 p.m. New York time

-

The Nasdaq 100 rose 0.7%

-

The Dow Jones Industrial Average was little changed

-

The MSCI World Index rose 0.3%

-

Bloomberg Magnificent 7 Total Return Index rose 0.8%

-

The Russell 2000 Index was little changed

Currencies

-

The Bloomberg Dollar Spot Index rose 0.1%

-

The euro fell 0.2% to $1.1054

-

The British pound fell 0.3% to $1.3125

-

The Japanese yen fell 0.8% to 146.11 per dollar

Cryptocurrencies

-

Bitcoin fell 0.5% to $59,222

-

Ether fell 0.2% to $2,534.84

Bonds

-

The yield on ten-year government bonds rose by four basis points to 3.90%

-

The German ten-year yield rose by two basis points to 2.30%

-

The British ten-year yield remained little changed at 4.02%

Raw materials

-

West Texas Intermediate crude fell 3.3% to $73.41 a barrel

-

Spot gold fell 0.7% to $2,502.91 an ounce

This story was produced with the help of Bloomberg Automation.

Most read from Bloomberg Businessweek

©2024 BloombergLP