Finance

Is macro making progress? – Ecolib

At a recent blogger conference, I was asked to name the most important paper published in my field (macroeconomics) in the past decade. I couldn’t think of any.

In a way, that’s a reflection of the fact that the field has evolved from the 20th century macro research with which I am most familiar. My ignorance may say more about me than it does about the macro field. Desperately, I suggested that Paul Krugman’s 1998 Brookings article (It’s Baack . . . ) was the most recent one that I remember having a decisive impact on the way we think about macroeconomics. A few years ago I wrote an article discussing how the important “Princeton School” of monetary economics was deeply influenced by this article.

Many brilliant economists continue to do some pretty sophisticated money/macro research. And yet I rarely see new articles that seem interesting to me, at least in the way that many articles from the last half of the 20th century seemed interesting when they were first published. And it’s not just macro. Casual art lovers like me know hundreds of famous paintings from the period 1880 to 1924, but very few famous paintings from the period 1980 to 2024. Why is that?

Tyler Cowen recently linked to an NBER working paper from Joel P. Flynn and Karthik Sastryx, which looks at how optimistic and pessimistic stories can contribute to the business cycle. On a technical level, the 134-page article far surpasses anything I’ve ever done, with literally hundreds of mathematical equations, some of them quite complex. Here is an excerpt from the conclusion:

When we fit the model to the data, we find that the cyclical implications of narratives are quantitatively significant: the measured declines in optimism account for about 32% of the peak-to-trough decline in output during the early 2000s recession and the recession. % during the Great Recession. Finally, we show that the interaction of many co-evolving and highly contagious narratives, some of which are individually sensitive to hysteresis, can nevertheless underlie stable fluctuations in emergent optimism and output. Taken together, our analysis shows that stories can be an important driver of the business cycle.

Their work uses a “real business cycle” framework, which I am generally somewhat skeptical about. It’s not that these RBC models don’t tell us important things about the economy. Rather, I believe that (at least in the US) real shocks are primarily important as a determinant of long-term trends, rather than business cycles. (With Covid being the obvious exception.)

I only skimmed the article, so I won’t comment on their empirical estimates, but this caught my attention:

Our analysis leaves at least two important areas open for future research. First, we analyzed how companies’ stories matter and moved away from studying households’ stories. It seems reasonable that similar mechanisms could operate on the household side of the economy, where contagious narratives could influence spending and investment decisions. Moreover, co-evolving narratives on both the ‘supply side’ and the ‘demand side’ of the economy can have mutually reinforcing effects. From this perspective, stories have the potential to explain even more of the business cycle than our analysis suggests.

I like this observation because I have long believed that the most important impact of (real) supply shocks is the way they interact with (nominal) demand shocks. So a real shock to the housing and banking sectors in 2007 probably pushed down the natural interest rate. The Fed fell behind the curve and cut rates too slowly (especially in 2008). This led to a drop in nominal GDP (less demand), making the recession much worse.

They conclude with the now almost obligatory call for further research:

Second, there is much more to study about what “makes a story a story” – that is, in the language of our model, what underlies the set of stories and their contagiousness? A richer study of these issues would shed more light on policy issues, including both the interaction of standard macroeconomic policies with narratives and the potential effects of directly ‘managing narratives’ through communications. Moreover, exploring these deeper origins of stories could enrich the study of narrative constellations beyond our analysis, to take into account the full economic, semantic, and psychological interactions between stories in a complex world.

Will further research provide answers to these questions? I’m sceptical. I worry that the next brilliant bunch of young macroeconomists will think to themselves, “Flynn and Sastryx have already done that, let’s develop a different model.” There’s probably enough truth in almost any plausible macro model that you can find some empirical support for the theory (at least if you ‘torture’ the data set enough).

It’s possible that my skepticism about modern macroeconomics is just a reflection of an old man out of touch with recent developments. I plead guilty. But in the second half of the twentieth century, you didn’t have to read hundred-page research articles to understand that macro produced many revolutionary ideas. I don’t see any interesting new ideas explained in non-technical articles for the layman.

Here’s a way to think about my pessimistic mindset. I have done macro research almost all my life. Quite early on I came to the conclusion that US business cycles were quite simple. In most cases (not Covid) it was simply a matter of monetary policy errors causing the NGDP swings, and real GDP being highly correlated in the short run due to persistent wage growth.

If you were going to explain why the paintings from 1880-1924 seem more memorable than the paintings from 1980-2024, you might point to the fact that painters of the earlier period discovered many interesting new styles, and they simply weren’t there. just as many interesting new styles to discover in the last period. Another view is that I am wrong and that future generations will discover even more masterpieces of painting from the period 1980-2024 than from 100 years earlier. Time will tell.

Thomas Kuhn said that we often make progress in science by developing models, then discovering that there are certain “anomalies” that cannot be explained by those models, and then developing new and improved models to explain those anomalies. Perhaps our best macro models from the late 20th century are quite good at explaining business cycles (and note that the ‘Fed error’ theory I just gave could explain why statement does not imply prediction). Perhaps the remaining anomalies are simply very difficult to explain.

But this doesn’t fully explain my skepticism about modern macro. You could say we invented it too many good macro models in the second half of the 20th century. We have Keynesian models, monetarist models, real business cycle models, Austrian models, MMT models and many variations within each category. Flynn and Sastryx use an RBC framework in their paper. Since my own view is that this framework is not very useful for understanding business cycles, this whole line of analysis seems a bit off from the outside. And from my perspective, that skepticism doesn’t just apply to RBC models each The non-market monetarist model somehow misses the point. It seems like they are all trying to explain something that has already been explained enough. They don’t address the anomalies in the model, where Fed mistakes drive the NGDP and create cycles due to persistent wages; they usually work with a completely different framework.

This is why, to a grumpy old man like me, macro no longer seems like it progressive. We don’t fill in the gaps; we are constantly trying to reinvent the wheel.

Again, it’s entirely possible that I’m out of touch. All I can say is that I no longer read articles and think, “I always wondered why certain macro variables (M, Y, P, i, U, etc.) showed this pattern, now it makes more sense.” I don’t see the progress.

Anyway, people in 1890 didn’t see Van Gogh’s genius yet, so it’s entirely possible I’m missing something important.

P.S. Here is a painting by Kandinsky from 1925. What was left to say?

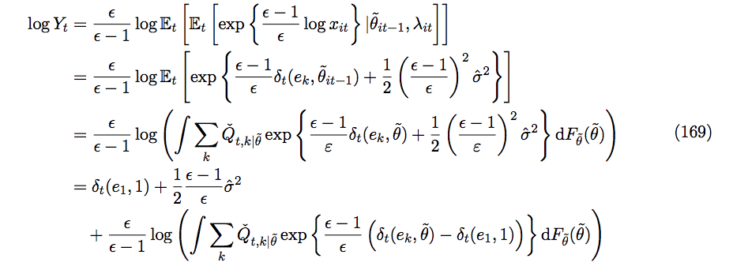

PPP. Here is one of the 247 mathematical equations in the article: