Finance

Powell is ready to keep the Fed on a higher and longer path

(Bloomberg) — Jerome Powell’s comments in the coming week will be closely analyzed by investors for clues about how long the Federal Reserve is willing to wait before cutting rates.

Most read from Bloomberg

The last time the US Federal Reserve chairman spoke, he indicated that policymakers are likely to keep borrowing costs high for longer than previously expected. He pointed to the lack of further progress in reducing inflation and the continued strength in the labor market.

The latest price data showing persistent underlying inflation, coupled with expectations for a robust employment report on Friday, is unlikely to prompt the Fed chief to change his tune.

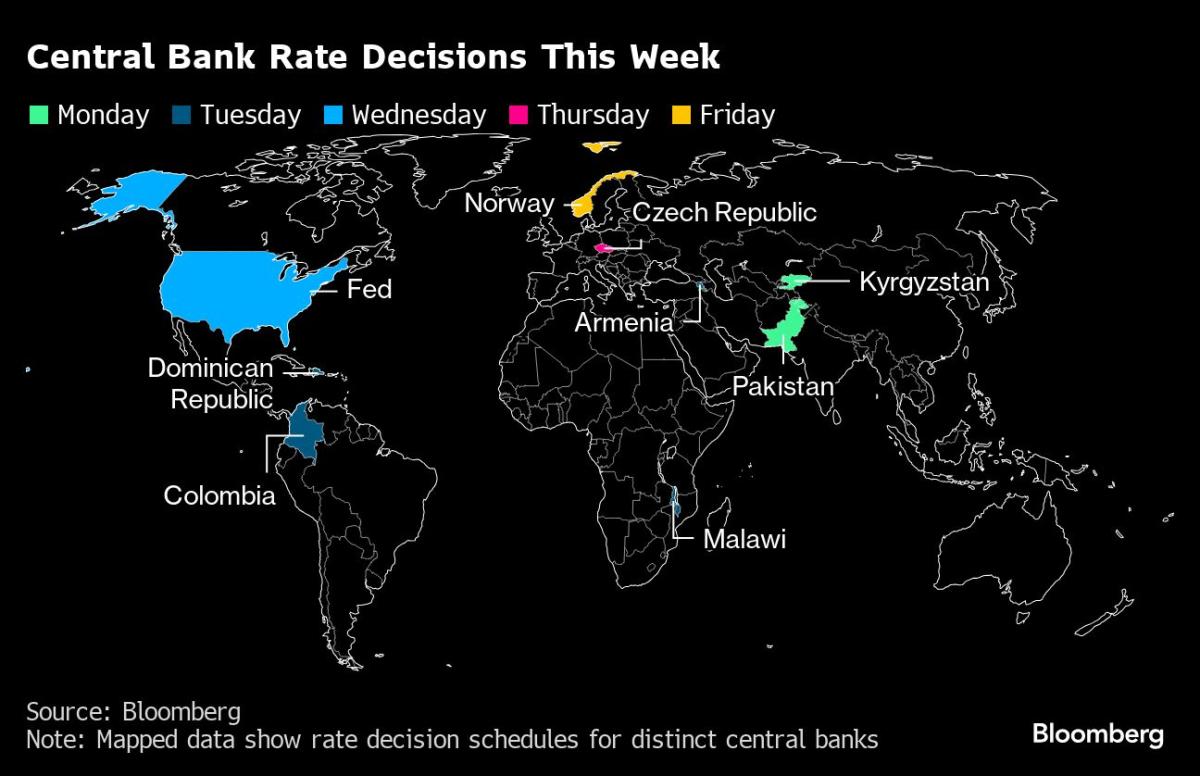

Powell will address reporters after the Fed’s interest rate decision on Wednesday, when the central bank is widely expected to keep borrowing costs at the highest level in more than two decades. Expectations for rate cuts have been pushed further to 2024, with investors now betting on up to two cuts by the end of the year.

Read more: Fed rate cut debate shifts from ‘when’ to ‘if’ based on inflation data

The week ends with the monthly jobs report, which offers a fresh look at the state of the U.S. labor market. Economists expect nonfarm labor cost growth to moderate to a still strong pace in April amid stable, low unemployment.

What Bloomberg Economics says:

“We expect Powell to make an aggressive pivot. At the very least, he will likely indicate that the average FOMC participant now expects “fewer” cuts this year. In a more aggressive direction, he could point to the likelihood that there will be no cuts – or even suggest that an increase is on the table, even if it is not the current basis.”

—Anna Wong, Stuart Paul, Eliza Winger & Estelle Ou, economists. For a full analysis, click here

We also get updates on a quarterly closely watched measure of labor costs, as well as monthly figures on vacancies and production.

Looking north, Canada’s gross domestic product figures for February could show a slight boost to the economy, giving the Bank of Canada options as it considers when to move to looser policies.

Elsewhere, Eurozone data could show that inflation is no longer slowing and the economy is starting to grow again, while Chinese surveys will point to the strength of expansion there. Central banks from Norway to Colombia will set interest rates, while the Paris-based OECD will release new global forecasts on Thursday.

Click here for what happened last week and below is our summary of what will happen in the global economy.

Asia

China shed light on its prospects for building on its first-quarter economic expansion with the release of official purchasing manager index data on Tuesday. The report will indicate whether manufacturing activity expanded for a second month in April.

There could be some seasonal weakness due to fewer business days, but the overall trend is likely to point to a continued recovery, according to Bloomberg Economics. On the same day, the Caixin gauge is expected, which has been hovering above the 50 mark for five months, which separates expansion from contraction.

Global trade will be in the spotlight as Australia, South Korea, Thailand, Sri Lanka and Vietnam all release trade figures during the week.

Japan will get a huge batch of data on Tuesday that is expected to show a recovery in industrial production in March, with retail sales and the unemployment rate also due to be released.

And South Korea’s consumer inflation data on Thursday is expected to show price growth will slow slightly while remaining above the Bank of Korea’s target, giving the central bank added incentive to delay any policy change.

Meanwhile, Thai Prime Minister Srettha Thavisin appointed capital markets veteran Pichai Chunhavajira as the country’s new finance minister, in an appointment that could ease tensions between the prime minister and the central bank over monetary policy.

Europe, Middle East, Africa

In the eurozone, data could show that the slowdown in inflation came to a halt in April for the first time this year. Consumer prices are likely to have risen by 2.4% year-on-year, consistent with March’s outcome, against the backdrop of rising energy costs.

The underlying metric that excludes such volatile items may reassure officials that the direction of travel is still downward, although national figures are likely to reveal some differences. Germany and Spain may have experienced faster inflation following the release of their figures on Monday.

The eurozone report will be released on Tuesday along with the latest GDP figures. Economists believe the region is likely to have returned to growth of at least 0.1% in the first quarter, after a shallow recession at the end of 2023.

As with inflation, Tuesday’s numbers may mask uneven outcomes across the region. To get a taste of that, investors are likely to pay close attention to Irish growth figures on Monday, which have a history of volatility.

Overall, the reports could echo European Central Bank President Christine Lagarde’s observation this month that the economy is weak and faces “bumps in the road” on the path of inflation.

Switzerland will release consumer price data on Thursday that could show inflation remains well below the central bank’s 2% ceiling target.

And the next day, investors in Turkey will be looking for progress in slowing consumer price growth.

Most of the market sees Turkish inflation continuing to rise in the coming months, from 68.5% to around 75% in March, despite almost a year of aggressive rate hikes. Until price increases subside, bond investors are unlikely to rush back into the lira bond market, a key target of the Turkish government.

Three monetary decisions take place in the wider region:

-

On Tuesday, Malawi officials may be convinced to raise the policy rate again to rein in inflation, which is likely to remain high due to crop damage caused by adverse weather conditions.

-

The Czech central bank will announce its latest decision on Thursday, with policymakers expected to cut borrowing costs by 50 basis points.

-

The next day, Norges Bank could leave deposit rates unchanged after the Norwegian economy developed better than expected, even as inflation fell faster than expected. Investors will be watching for indications that policymakers are becoming more cautious when it comes to lowering borrowing costs in the fall.

Latin America

Preliminary first-quarter Mexican production figures are likely to show that the economy contracted slightly in the three months through December. The consensus among analysts is that growth will slow for a third year in 2023, from 3.2% in 2023 to roughly 2.4%.

Brazil will publish a number of reports, including the broadest measure of inflation, the central bank’s expectations survey, the current account, industrial production and the national unemployment rate.

Since last June, unemployment in Latin America’s largest economy has been below 8%, which many Brazil watchers see as the economy’s unaccelerated unemployment rate.

Chile releases a slew of indicators for March, including retail sales, unemployment, industrial production, manufacturing, copper production and GDP proxy figures. Stronger-than-expected growth and a rebound in inflation prompted the central bank to slow the pace of easing earlier this month.

In Peru, the April inflation report for the megacity Lima could finally see prices back within the 1% to 3% tolerance range, while still above the 2% target.

Colombia’s central bank is widely expected to extend its easing cycle with a second consecutive half-point cut, which would lower the policy rate to 11.75%, amid a steady process of disinflation. BanRep will also publish its quarterly inflation report, updating growth and inflation forecasts and presenting a revised monetary policy outlook.

–With help from Paul Wallace, Ott Ummelas, Robert Jameson, Laura Dhillon Kane, Vince Golle, Patrick Donahue, Brian Fowler and Monique Vanek.

(Updates with tout after fourth paragraph)

Most read from Bloomberg Businessweek

©2024 BloombergLP