Finance

What you need to know this week

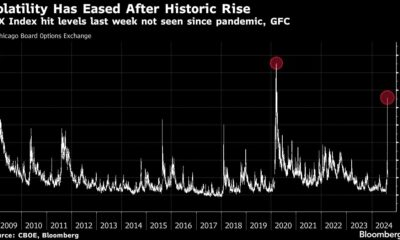

Wall Street’s busiest week of the summer sent stocks tumbling after a weak July jobs report highlighted concerns about the health of the U.S. economy and gains from the Big Tech sector failed to calm fears away from investors.

The S&P 500 (^GSPC) fell more than 2.5% this week, while the Nasdaq Composite (^IXIC) fell more than 3.7%. This decline in the Nasdaq sent the index into a correction after it closed down more than 10% from its last high on July 10. Meanwhile, the Dow Jones Industrial Average (DJI) also fell about 2.5%.

The week ahead won’t provide much new macroeconomic fodder for investors, with updates on service sector activity and weekly jobless claims expected to be the main releases.

On the business front, earnings from Airbnb (ABNB), SuperMicro Computer (SMCI), Disney (DIS) and Eli Lily (LLY) highlight another busy week of quarterly updates.

A deep cut

After months of shaky sentiment about when the Federal Reserve will cut rates, the market appears to have reached a consensus: the Federal Reserve will cut rates next month.

A recent string of softer-than-expected economic data now has investors wondering how big that cut will be.

A slew of weaker-than-expected economic data, highlighted by the July jobs report, which spawned a closely watched recession indicator, has fueled speculation that the Fed’s current policy rate may be far too restrictive.

“Even if the softening in labor market conditions tapers off from here, it appears the Fed is offside by at least 100 basis points, probably more,” Michael Feroli, JPMorgan’s chief U.S. economist, wrote in a note to clients on Friday. “So we now think the FOMC will cut 50 bps at both the September and November meetings, followed by a 25 bp cut at each meeting thereafter.”

At his most recent news conference, Fed Chairman Jerome Powell declined to specify when the Fed plans to cut rates, but noted that “September is on the table.”

This confirmed the market’s preconception at the meeting that there would be an easing of policy by the end of the summer. With a September rate cut fully priced in, the new market debate has shifted to how much the Fed will cut and which data points will drive this shift.

Feroli added that from a risk management perspective, there is a strong case for the Fed to make cuts before the September meeting.

But, he wrote, “Maybe Powell doesn’t want to add more noise to what has already been a summer of events.”

As of Friday afternoon, markets had priced in a roughly 70% chance that the Fed would cut rates by 50 basis points, compared to a 12% chance the week before. according to the CME FedWatch Tool.

This shift will likely put a spotlight on upcoming comments from Federal Reserve officials. Federal Reserve officials Austan Goolsbee, Mary Daly and Tom Barkin will make public appearances in the coming week.

Disney’s streaming in the spotlight

Disney headlines quarterly earnings week when it reports earnings Wednesday morning.

The focus remains on the state of Bob Iger’s turnaround strategy for the entertainment giant, as the company doubles down on its commitment to expensive sports rights.

The NBA recently secured a media rights package worth approximately $77 billion more than 11 years with new partners including tech giant Amazon (AMZN) and Comcast’s NBCUniversal (CMCSA), as well as Disney.

“We think investor attention will turn to Disney+ and the progress management has made in pushing technology, with a focus on combating churn and improving the user experience,” CFRA analyst Ken Leon wrote in a note previewing the release. “A faster path to significant gains would be a plus for the direct-to-consumer segment.”

Leon added: “Sports rights and the hefty offer to broadcast the NBA should be included on the earnings call.”

Revenue Scorecard

While shifts in the macroeconomic story took center stage and weighed on markets last week, the S&P 500 as a whole is quietly posting its best quarterly annualized earnings growth in nearly three years.

Now that 75% of the S&P 500 have reported results, the index expects earnings growth of 11.5% year over year, according to FactSet senior earnings analyst John Butters.

This would be the highest year-over-year earnings growth reported by the index since the fourth quarter of 2021.

Looking ahead, analysts cut their third-quarter earnings estimates by 1.8% in the first month of the quarter, in line with the average cut over the past two decades.

Weekly calendar

Monday

Economic data: S&P Global US Services PMI, July final (56 expected, 56 prior); S&P Global US Composite PMI, July final (55 earlier); ISM Services Index (51.3 expected, 48.8 previously)

Income: Avis Budget Group (CAR), Clover (CLOV), Hims & Hers Health (HIMS), Lucid (LCID), Palantir (PLTR), Simon Property Group (SPG), Tyson (TSN)

Tuesday

Economic data: Trade balance, June (-$72.6 billion expected, -$75.1 billion previously)

Income: Airbnb (ABNB), Amgen (AMGN), Caterpillar (CAT), Celsius Holdings (CELH), Constellation Energy (CEG), Devon Energy (DVN), Reddit (RDDT), Rivian (RIVN), Super Micro Computer (SMCI), Uber (UBER), Wynn Resorts (WYNN)

Wednesday

Economic data: MBA mortgage applications, week ending August 2 (-3.9% prior); Consumer Credit, June ($10.30 billion, previously $11.35 billion)

Income: CVS Health (CVS), Disney (DIS), Dutch Bros (BROS), Lyft (LYFT), Novo Nordisk (NVO), Occidental Petroleum (OXY), Robinhood (HOOD), Shopify (SHOP), Sony (SONY)

Thursday

Economic data: Initial unemployment claims, week ending August 3 (previously 249,000); Continued claims, week ending July 27 (1.87 million previously); Wholesale inventories month-on-month, June final (+0.2% expected, +0.2% earlier)

Income: Datadog (DDOG), Eleven Beauty (ELF), Eli Lily (LLY), Novavax (NVAX), Paramount (PARA), Plug Power (PLUG), SoundHound (SOUN), The Trade Desk (TTD)

Friday

Economic data: No significant economic figures.

Income: Canopy Growth (CGC), Nikola (NKLA)

Josh Schafer is a reporter for Yahoo Finance. Follow him on X @_joshschafer.

Click here for an in-depth analysis of the latest stock market news and events affecting stock prices

Read the latest financial and business news from Yahoo Finance