Finance

Why the minimum wage and some tax benefits do not budge despite inflation

Martin Barraud | Ojo images | Getty Images

Many Americans are probably familiar with financial thresholds that are adjusted each year for inflation.

They include contribution limits for 401(k) plans, cost-of-living adjustments for Social Security benefits and federal income tax brackets, to name a few.

These adjustments will help households keep pace with the rising cost of living.

For example, without adjustments, more and more households would move into higher tax brackets over time and the purchasing power of social security beneficiaries would decline.

But some thresholds, such as the federal minimum wage, are not inflation-adjusted.

What is and is not indexed to inflation depends largely on the whims of lawmakers when they drafted the relevant legislation, said Bill Hoagland, senior vice president at the Bipartisan Policy Center. “It’s all over the map,” he said.

Inflation adjustments can be a “double-edged sword,” said Mark Zandi, chief economist at Moody’s Analytics.

In times of high inflation, such as in 2022, the lack of an adjustment “could quickly become a financial problem” for households, Zandi said.

However, if everything were indexed, it would be harder “to put inflation back in the bottle when all goes well,” he added.

Here are some common thresholds that do not have an annual inflation adjustment.

Minimum wage

The federal minimum wage – $7.25 per hour – has remained unchanged since 2009.

That’s the longest period in history without a hike from Congress, according to the Economic Policy Institute, a left-leaning think tank.

The minimum wage has lost 29% of its value since 2009, after taking into account the rising cost of living, according to an EPI analysis. It’s worth less than at any time since February 1956, the group found.

That said, only 1.3% of all US hourly workers (about 1 million people in total) were paid wages at or below the federal minimum in 2022, according to the Bureau of Labor Statistics. That is “well below” the 13.4% share in 1979, the report said.

Thirty states plus the District of Columbia have adopted a higher minimum for employees. In addition, 58 places raised their minimum above that of their state, according to the EPI.

The minimum wage is indexed for inflation in 19 of the states plus DC, according to the EPI.

Social Security Taxes

The federal government began taxing Social Security benefits in 1984.

Social Security benefits are taxed at the federal level once the beneficiary’s income exceeds a certain dollar level. Up to 85% of their benefits may be taxable. (This is explained in more detail below.)

The dollar thresholds are not adjusted for inflation and Congress has never changed them.

More from Personal Finance:

Flying will be cheaper in 2024. But not for some destinations

Why groceries are so expensive

Why it can be expensive to use cash via a credit card

Since U.S. benefits and other income have increased, the share of beneficiaries paying federal income tax on their benefits has increased over time, according to the Social Security Administration.

Less than 10% of families paid federal income taxes on their benefits in 1984.

The share has increased significantly: the SSA estimates about 40% of people who receive Social Security must pay federal income taxes on their benefits.

The federal government uses a specific income formula to determine whether benefits are taxable. This “combined income” formula is: adjusted gross income + non-taxable interest + half of your Social Security benefits.

For example, individual tax returns would pay taxes up to 50% of their benefits if their combined income is between $25,000 and $34,000. Up to 85% may be taxable if income exceeds $34,000.

Couples filing jointly would pay taxes on up to 50% of their benefits if their combined income is between $32,000 and $44,000. Up to 85% may be taxable if income exceeds $44,000.

Investments for the rich

Americans generally must be “accredited” to invest in private companies and investments such as private equity and hedge funds.

To qualify, households must meet certain requirements, such as a minimum net worth or annual income.

It is a matter of consumer protection: the thresholds goal Buyers are financially sophisticated and can bear the risk of loss from private investments, according to the Securities and Exchange Commission.

Individuals can generally become accredited by having an annual income of $200,000, or $300,000 for married couples. Individuals or couples may also qualify with a total net worth of $1 million, not including the value of their primary home.

However, these dollar thresholds have not changed since their inception in the early 1980s.

According to SEC data, only 1.5 million households – 1.8% – qualified as accredited investors in 1983.

More than 24 million American households – about 18.5% of them – qualified in 2022the agency said in a December report.

Tax deduction for homeowners

Many common tax benefits, such as the standard deduction, receive an annual inflation adjustment.

But others don’t. An example of this is the tax deduction for mortgage interest.

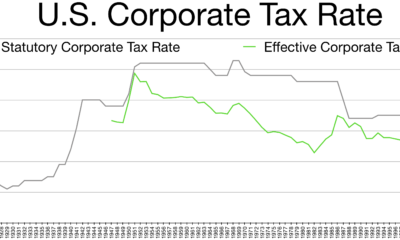

A 2017 tax law signed by President Donald Trump limited the deduction for mortgage interest on the first $750,000 of new mortgage debt. The limit was previously $1 million. (Neither are pinned down to inflation.)

In 2026, that threshold will return to $1 million without congressional action.

There are now a record number of U.S. cities where the “typical” home is worth $1 million or more, according to a recent Zillow survey.

Net investment income tax

Certain taxpayers must pay a 3.8% surcharge on their investment income.

This “net investment income tax,” also known as the Medicare surcharge, generally applies if modified adjusted gross income exceeds $200,000 for single tax filers or $250,000 for married joint filers.

The tax is largely paid by high-income households, according to the Congressional Research Service.

However, because the dollar thresholds are not indexed to inflation, “more taxpayers are subject to the tax over time, regardless of whether their real (inflation-adjusted) income has risen or increased significantly,” the CRS wrote.